My Account >> Market Comment for 09/27/2022 (Closing)

CORN COMMENTS

NO NEW RECOMMENDATIONS

Corn futures could not hold morning strength, finishing between 3/4 of a cent lower and 2 1/2 cents higher under pressure from renewed strength in the dollar and increasing Midwest harvest activity. An absence of fresh demand news and ongoing concerns about rising interest rates were also negative market factors. Corn futures had rallied in morning trade helped by a weaker dollar, but faded as the dollar index recovered and turned higher. Most-active Dec. corn edged up 1 1/4 cents to $6.67 1/2, while March corn rose 2 cents to $6.72 3/4 and Dec. 2023 corn fell 3/4 of a cent to $6.10 1/4.

Clearly, corn futures did not finish the session well from a technical standpoint, and this morning's strength appears to have been just a modest Tuesday correction. Nearby Dec. futures finished 10 1/2 cents off their session high and appear set to break out the bottom of their recent trading channel at $6.66 1/2, which could set up a quick retreat to the $6.50 level and would open further downside risk back to $6.00. Nearby resistance for Dec. is at $6.68-$6.69. Dec. 2023 futures ended 8 1/2 cents off their session high and look poised to test support at $6.00. A close below $6.00 would open downside risk to at least $5.75. Dec. 2023 has nearby resistance at $6.18 3/4.

While corn harvest has gotten off to a sluggish start, keeping supplies tight in the cash market, with 58% of the U.S. crop mature as of Sunday, harvest activity should be picking up considerably. Only 47% of the Illinois crop was mature by Sunday, well behind the 5-yr. avg. of 66%, but 63% of the Iowa crop was mature, ahead of the avg. pace of 61%.

Scattered light rains have moved through parts of the eastern Corn Belt today, but weather forecasts continue to be very favorable for harvest activity. The NWS 6- to 10-day and 8- to 14-day forecasts both favor below-normal precipitation across the entire Corn Belt, with above-normal temperatures across most of the region.

Central Illinois processor spot corn basis bids are steady, ranging from 15 under Dec. futures to 45 over, according to USDA. CIF basis bids for delivery of corn to the U.S. Gulf are steady to stronger vs. Monday afternoon with the spot bid up strongly again as corn supplies at the Gulf remain tight amid the sluggish start to harvest. The CIF bid for September delivery is 10 cents stronger at 150 over Dec. futures, with the bid for October delivery 4 cents stronger at 124 over, while the bid for November delivery is steady at 112 over.

SOYBEAN COMMENTS

NO NEW RECOMMENDATIONS

Like corn futures, soybean futures could not hold early strength and wound up 3 1/4 cents lower to 1/2 cent higher after the dollar index recovered from morning weakness. Slower-than-expected U.S. harvest progress also provided support for soybean futures, but that faded amid expectations for a rapid pick up in harvest activity with forecasts calling for favorable harvest weather. An absence of fresh export demand and forecasts calling for beneficial rains in Brazil's key growing areas were also negative market factors. Most-active Nov. soybean futures fell 3 1/4 cents to $14.08, while Jan. futures fell 2 1/4 cents to $14.14. Dec. soyoil dropped 7 points to 62.39 cents, while Dec. soymeal futures fell $3.90 to $413.60.

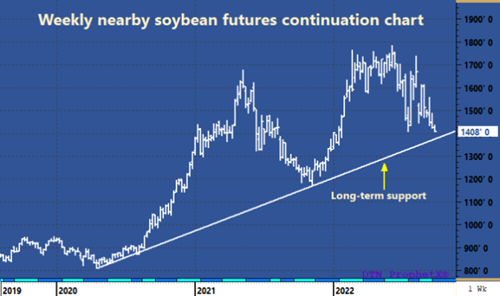

Soybean futures put in an even weaker close than corn futures again, with nearby Nov. futures settling 29 1/4 cents off their session high and posting an outside day down, suggesting they may be set to accelerate lower. A drop through $14.00 by Nov. should set up a test of the long-term support line across the 2020 and 2021 lows on the weekly nearby soybean futures continuation chart, which we peg at about $13.78. A breakout below that support line would look quite bearish technically.

While we still have a difficult time seeing a huge downside for soybean prices given the tight U.S. carryout forecast, that forecast is not set in stone. The U.S. crop size is still not clear and USDA's demand estimates could high in light of the economic outlook. The negative threat of an economic recession combined with potential for a huge Brazilian crop is not something to be ignored.

As noted in corn comments, Midwest weather favors strong harvest progress over the next two weeks. Meanwhile. Brazil's center-west and center-south are still expected to receive significant rain in the coming week with some periodic follow up shower activity expected next week. A little too much rain will fall in Mato Grosso do Sul, Parana, Sao Paulo and far southern Minas Gerais where delays to farming activity will occur, but the moisture will be good for long term crop prospects.

Nationwide, 1.7% of Brazil's 2022-23 soybean crop had been planted as of Sept. 24, compared with 1.0% last year, according to CONAB, the supply dept. of Brazil's agriculture ministry. In Parana state, 9% of the crop has already been planted compared with only 3% a year ago, the state agricultural economics department said today.

Central Illinois processor spot soybean basis bids are steady to 60 cents weaker at 10 to 30 over Nov. futures, according to USDA. CIF basis bids for delivery of soybeans to the Gulf are steady to slightly stronger vs. Monday afternoon. The bid for September delivery is 1 cent stronger at 206 over Nov. futures, with the bid for October delivery steady at 142 over, while the bid for November delivery is steady at 136 over.

WHEAT COMMENTS

NO NEW RECOMMENDATIONS

Wheat futures ended higher, ending a two-session losing streak with support from the volatile situation in Ukraine and outside markets. Chicago wheat was up 12 to 13 cents, settling at $8.71 ½ in the December, $8.84 ¼ in the March and $8.90 ½ in the May. Kansas City wheat was up 13 to 15 cents, settling at $9.43 ¼ in the December, $9.40 ½ in the March and $9.38 ½ in the May. Minneapolis wheat rose 9 to 12 cents, settling at $9.43 ¼ in the December, $9.48 in the March and $9.51 ¼ in the May. Gains in corn and soybeans, along with a pause in the dollar's rally, helped wheat to climb today.

The war in Ukraine, and more broadly between Russia and the West, shows no signs of de-escalation, which is feeding concern about Ukraine grain exports out of the Black Sea and whether Russia might cancel that deal. As we have noted there have been three drone attacks on the key port city of Odesa in the past week. And today there was a leak detected in the Nord Stream natural gas pipeline in the Baltic Sea, which European leaders are saying is an act of sabotage. The leaks will not have a direct impact on natural gas supplies in the near-term, as Russia had cut off supplies anyway, but if it is an act of sabotage it represents another escalation between Russia and the West.

Drought conditions in a large portion of the U.S. HRW wheat belt remain a supportive market factor, while favorable winter wheat planting progress is a negative factor. A huge Russian crop also continues to cap wheat market strength. Russia and Afghanistan's Taliban government agreed today on a deal to send some Russian wheat there.

Planting is just getting underway in Midwest SRW wheat growing areas. Illinois planting progress was put at 1% as of Sunday vs. the 5-yr. avg. of 3%, with progress at 4% in Indiana vs. an avg. pace of 8% and progress in Ohio at 2% vs. an avg. pace of 8%. No progress was reported in Missouri vs. an avg. of 3%.

European Union soft wheat exports for 2022/23 (July-June) totaled 8.80 MMT as of Sept. 25, up slightly from 8.75 MMT a year earlier, according to European Commission data. However, the Commission again said the export data may be incomplete.

COTTON AND RICE COMMENTS

NO NEW RECOMMENDATIONS

Cotton bulls had a little space to breathe today as pressure from outside financial markets abated a little, but cotton futures still ended slightly lower. December cotton settled down 28 pointes to 88.09, after trading a range of 87.55 to 91.85. March cotton was down 55 points to 85.39. It's the fourth straight day cotton has ended lower. The market again made new 10-week lows, and there's no clear technical support above the major July lows, which in the December contract is at 82.54.

The big weather story for the next couple of days is Hurricane Ian. The latest storm track has moved a little to the east, which means greater damage to citrus and sugarcane areas of central Florida, but less damage to cotton in the Southeast, according to World Weather Inc. In particular, Georgia is now likely to miss the heart of the storm, though cotton-growing areas will still see unwelcome rains. Says World Weather: “Cotton fiber quality issues are expected in the Carolinas and a part of Georgia, but no serious production losses are expected with this new path.”

USDA on Monday afternoon said that 67% of the crop nationally had reached the bolls opening stage, including three-quarters of Georgia's crop. The harvest is 15% done nationally, up from 11% last week, and the five-year average of 14%. The Texas crop was 25% harvested, up from 20% the prior week and the five-year average of 21%.

Rice futures ended slightly lower in light trading volume. November rice was down 3 ½ cents to $17.31 ½, after trading a range of $17.26 ½ to $17.55. January rice was down a penny to $17.61 1/2. Harvest pressure is a negative factor, and so far yields in Arkansas are coming in at or above expectations.

The U.S. harvest was 59% done as of Sunday per USDA, up from 45% the prior week and near the average of 63%. In Arkansas the harvest was 61% done, up from 41% the prior week and just off the average of 66%.

LIVESTOCK COMMENTS

LIVESTOCK COMMENTS

NO NEW RECOMMENDATIONS

Live cattle futures ended mostly lower, with the exception of nearby October, which settled up 10 cents to $143.575. Other contracts were down 45 to 80 cents, with continued pressure from a weaker stock market and concerns about an economic recession. December closed at $146.50, and February settled at $150.85. The afternoon Boxed Beef report showed Choice up 59 cents and Select down $2.14.

There was some light/moderate trade in Kansas and Texas today, with USDA reporting a price of $143 in both states, which is steady with a week ago. Some asking prices are also reported in the southern Plains at $145, but asking prices are not well established. No trade in Nebraska reported today. Beef packer operating margins continue to slowly shrink with the avg. margin estimated at only $19.95 per head, down from Monday on $28.70.

Feeder cattle futures were also lower. September feeders lost $1.175 to $175.70, compared to a CME Feeder Cattle Index that was at $177.82 yesterday. October feeders settled at $176.125 and November closed at $176.275.

Lean hog futures continued to plummet, falling amid weaker pork prices and demand concerns as traders await Thursday's Hogs and Pigs report. October settled down $1.675 to $88.70, December was down $3.15 to $76.25, and February was down $3.30 to $80.35. Dec. and Feb. futures hit their lowest level since last winter. The afternoon pork carcass cutout value was down $2.45.

Futures are now becoming technically oversold going into Thursday's USDA quarterly Hogs and Pigs report, but show no signs they are near a bottom. We may consider taking hedge profits, though, on any near-term bounce. Dec. futures are again sharply discount to cash, with the CME cash lean hog index is 60 cents lower at $96.66. The average pork packer operating margin is estimated at $6.35 per head, down from $15.00 on Monday. Today's slaughter is expected to run 482,000 head, vs. 485,000 head last week and 473,000 last year.

BROCK MARKET POSITIONS:

CORN: Cash-only Marketers: 2021 CROP: 100% sold (9-24-20, 11-30-20, 2-25-21, 4-27-21, 4-29-21, 5-21-21, 11-3-21, 11-30-21, 12-29-21, 2-3-22, 2-25-22, 3-16-22). 2022 CROP: 60% sold on hedge-to-arrive and regular forward contracts (11-30-21, 1-6-22, 2-3-22, 3-16-22, 5-4-22, 6-1-22, 8-24-22, 9-22-22). 2023 CROP: 5% sold on a hedge-to-arrive contract against Sep. 2023 futures (5-5-22)

Hedgers: 2021 CROP: 100% cash sold (9-24-20, 11-30-20, 2-25-21, 4-27-21, 4-29-21, 11-3-21, 11-30-21, 12-29-21, 2-3-22, 2-25-22, 3-16-22).

2022 CROP: 55% cash sold on hedge-to-arrive contract and regular forward contracts (11-30-21, 2-3-22, 3-16-22, 3-28-22, 5-4-22, 6-1-22, 8-24-22, 9-22-22); long 1 $5.50 put option on Dec. 2022 futures/short 1 Dec. 2022 $6.70 call option on 10% of expected production (11-5-21, 3-2-22); aside futures. 2023 CROP: 5% sold on a hedge-to-arrive contract against Sep. 2023 futures (5-5-22), long $6.60 Oct. put options on Dec. 2022 futures against 10% (9/9/22), aside futures.

SOYBEANS: Cash-only marketers: 2021 CROP: 100% sold on hedge-to-arrive and regular forward contracts (9-24-20, 11-30-20, 2-26-21, 4-27-21, 4-29-21, 5-21-21, 10-1-21, 11-4-21, 12-29-21, 2-3-22, 2-14-22, 2-25-22). 2022 CROP:50% forward contracted (10-1-21, 1-6-22, 2-25-22, 4-25-22, 5-4-22, 6-22-22, 8-24-22). 2023 CROP: 5% sold on a hedge-to-arrive contract (5-4-22).

Hedgers: 2021 CROP: 100% cash sold on hedge-to-arrive and regular forward contracts (9-24-20, 11-30-20), 2-26-21, 4-27-21, 4-29-21, 5-21-21, 10-1-21, 11-4-21, 12-29-21, 2-3-22, 2-14-22, 2-25-22). 2022 CROP: 50% forward contracted in the cash market (10-1-21, 1-6-22, 2-25-22, 4-25-22, 5-4-22, 6-22-22, 8-24-22), aside futures. 2023 CROP: 5% cash sold on a hedge-to-arrive contract (5-4-22).

SRW WHEAT: Cash-only Marketers: 2022 Crop: 65% sold on forward contracts and hedge-to-arrive contracts (8-5-21, 12-28-21, 2-25-22, 3-7-22, 3-16-22, 4-20-22, 6-1-22, 9-16-22, 9-21-22). 2023 CROP: 15% sold on hedge-to-arrive contracts (11-5-21,4-29-22).

Hedgers: 2022 Crop: 65% sold on forward contracts and hedge-to-arrive contracts (8-5-21, 12-28-21, 2-25-22, 3-7-22, 3-16-22, 4-20-22,6-1-22, 9-16-22, 9-21-22); aside futures. 2023 CROP: 15% sold on hedge-to-arrive contracts (11-5-21, 4-29-22), aside futures.

HRW WHEAT: Cash-only Marketers: 2022 Crop: 65% sold on forward contracts and hedge-to-arrive contracts (8-5-21, 12-28-21, 2-25-22, 3-7-22, 3-16-2022, 4-20-22, 6-1-22, 9-16-22, 9-21-22). 2023 CROP: 15% sold on hedge-to-arrive contracts (11-5-21, 4-29-22).

Hedgers: 2021 CROP: 2022 Crop: 65% sold on forward contracts and hedge-to-arrive contracts (8-5-21, 12-28-21, 2-25-22, 3-7-22, 3-16-22,5-20-22, 6-1-22, 9-16-22, 9-21-22); aside futures. 2023 CROP: 15% sold on hedge-to-arrive contracts (11-5-21, 4-29-22), aside futures.

LEAN HOGS: Short Dec. 2022 lean hog futures on 25% of 4th qtr. marketings (9-21-2022); short Feb. 2023 futures on 25% of 1st qtr. marketings (9-22-22).

LIVE CATTLE: Short Dec. 2022 live cattle futures on 25% of 4th qtr. marketings (9-22-22); short Feb. 2023 live cattle futures on 25% of 1st qtr. marketings (9-22-22).

FEEDER CATTLE: Buyers are aside futures and sellers remain aside futures.

MILK: Aside futures. No cash forward contracts advised.

FEED BUYERS: CORN: No forward coverage in place. SOYMEAL: No forward coverage in place.

COTTON: Cash-only Marketers: 2021 CROP: 100% sold (12-16-20, 2-10-2021, 2-23-21, 7-30-21, 8-17-21, 9-9-21, 9-27-21, 10-18-21, 1-5-22, 2-14-22, 2-25-22). 2022 CROP: 40% forward contracted (9-27-21, 11-19-21, 2-14-22, 4-14-22).

Hedgers: 2021 CROP: 100% cash sold(12-16-20, 2-10-21, 2-3-21, 7-31-21, 8-17-21, 9-9-21, 9-27-21, 11-3-21, 1-5-22, 2-14-22, 2-25-22). 2022 CROP: 40% forward contracted (9-27-21, 11-19-21, 2-14-22, 4-14-22); long 1 95-cent put option on Dec. 2022 cotton futures (1-25-22); short 1 Dec. 80-cent put option against 20% of expected production (1-25-22).

RICE: 2021 CROP:100% cash sold (5-14-21, 7-12-21, 8-19-21, 9-27-21, 11-19-21, 1-5-22, 3-2-22, 5-16-22, 6-1-22). 2022 CROP: 50% cash forward contracted (3-2-22, 3-8-22, 4-20-22, 6-1-22, 8-18-22).

NOTE: Along with the potential for profit, there is always a risk of losing money when trading futures and options contracts.

Copyright 2019 by Richard A. Brock & Associates, Inc.

Any unauthorized redistribution or reproduction of this commentary is strictly forbidden.